Credit Scores Demystified: What Really Matters

Confused by credit scores? Learn the factors that truly move your number—and what doesn't—plus practical steps to build and protect it.

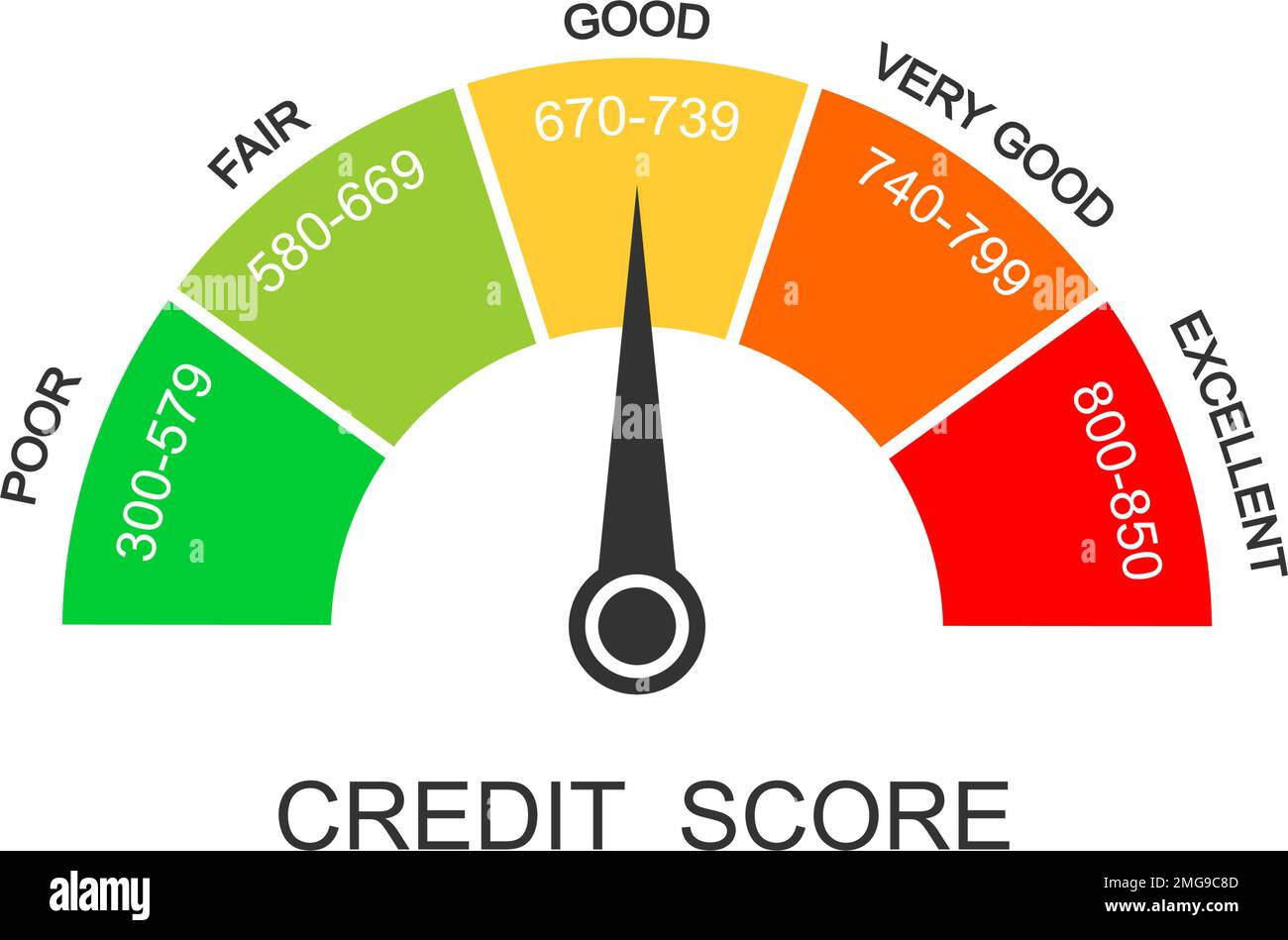

Credit Score Basics

A credit score is a three digit summary of how reliably you manage borrowed money, distilled from your credit reports and interpreted by scoring models. Lenders, landlords, and even some insurers use it to estimate the likelihood you will pay as agreed. While formulas vary, most models focus on a few core ingredients: payment history, amounts owed and credit utilization, length of credit history, credit mix, and new credit. There is no magic shortcut or insider hack; solid habits practiced consistently are what move the needle. Think of your score as a living snapshot, updated as creditors report. That is why accuracy matters. Reviewing your reports for errors, understanding what each account represents, and knowing how balances are captured can prevent surprises. Your goal is not to chase a perfect number, but to build a durable profile that saves money on interest, grants access to better products, and supports resilience in your personal finance plan over time.

Payment History The Heavy Hitter

Nothing influences your score more than on time payments. A single 30 day late mark can dent your profile, and deeper delinquencies like 60 or 90 days past due can sting even more. Models read missed payments as elevated risk, so prevention is paramount. Put bills on autopay for at least the minimum, then pay in full when possible to avoid interest. Use calendar reminders, stack due dates near payday, and watch for statement cutoffs so your activity is reported as expected. If you run into trouble, call your lender early to request a hardship plan, payment deferral, or a structured catch up schedule. After resolving an isolated mistake, some creditors may consider a goodwill adjustment, especially when you show a strong history. Keep documentation, track every conversation, and avoid repeat issues. Over time, a spotless streak of consistent payments can overshadow past missteps, reinforcing the most powerful message your score can send to any future lender.

Balances and Utilization The Leverage You Control

Your credit utilization ratio measures how much of your revolving limits you are using, and it is a major driver of scores. Lower tends to be better, because it signals breathing room and disciplined spending. Even if you pay your cards in full, the statement balance often gets reported, so high usage during the cycle can still appear as heavy utilization. Consider mid cycle payments to nudge reported balances lower, or request a credit limit increase without a hard inquiry when appropriate. Spreading expenses across multiple cards, timing large purchases after a statement closes, and avoiding maxing out a single line can smooth the ratio. Be cautious about closing unused cards, since losing available credit may spike utilization. If you become an authorized user on a responsible account with low balances and a long history, you might benefit from its profile, though misuse can also hurt. Thoughtful day to day management here provides quick, tangible scoring wins.

Age, Mix, and New Credit The Long Game

The length of credit history reflects how long your accounts have been active and the average age across them. Older, well maintained lines show stability, so keeping no fee cards open and lightly active can help maintain age. Your credit mix looks at the types of accounts you manage, such as revolving cards and installment loans. A healthy mix can add nuance to your profile, but never borrow just to chase points. When you apply for new credit, hard inquiries and young accounts may temporarily trim your score. That short term dip often fades as you demonstrate good behavior. For rate shopping on big loans, applications grouped into a tight window are often treated as a single intent, reducing impact. Use prequalification tools that rely on soft inquiries to survey options without adding dings. Patience turns these factors into allies, as time and steady habits compound the credibility of your profile.

What Does Not Count As Much As You Think

Many assumptions about credit scoring miss the mark. Your income, job title, savings balance, and education are not scoring factors, even though lenders consider affordability separately. Demographics such as age, race, religion, or marital status are not used. Soft inquiries like checking your own score do not affect it. Debit card activity, cash transactions, and most utility or rent payments typically do not help unless they are reported as tradelines through specific services or arrangements. Closing an account is not inherently negative, but it can indirectly hurt by raising utilization or shrinking your average age. Likewise, carrying a balance does not boost scores; it only adds interest. A thin file with few accounts is not a penalty by itself, yet limited data can make risk harder to gauge. Focus on what truly matters in the models, and let myths go, so your energy targets actions with measurable scoring impact.

Practical Playbook Building Repairing and Protecting

Start by auditing your credit reports for accuracy, then file disputes on errors with clear evidence. If you are building or rebuilding, consider a secured card or a credit builder loan that reports to all major bureaus, and use it consistently with low utilization and on time payments. Becoming an authorized user on a trusted person account with strong history can jump start your file, provided the primary user keeps balances modest and pays on time. Pay statement balances in full to avoid interest, or at least cover well above the minimum. Space out applications to limit hard inquiries, and plan months ahead of major borrowing so your profile is in peak shape. Enable alerts for due dates and unusual activity, and consider a credit freeze to block unauthorized accounts. Improvement is rarely instant, but steady, boring excellence beats quick fixes. With patience, your score becomes a durable asset that quietly lowers costs across your personal finance life.