Index Funds Explained: A Simple Path to Investing

Learn how index funds offer low-cost diversification, track the market, and help beginners invest simply, with steps, fees to watch, and tips to start.

What Is an Index Fund?

An index fund is a pooled investment vehicle designed to mirror the performance of a specific market benchmark, such as a broad stock or bond index. Instead of relying on a manager to pick winners, it follows a passive investing approach: it buys the same types of securities, in similar proportions, that exist in the chosen index. This structure delivers built-in diversification, because a single purchase spreads your money across many companies or issuers at once. Diversification can reduce the impact of any one holding on your overall results, smoothing the ride through market ups and downs. Another key feature is a typically low expense ratio, the ongoing fee that covers fund operations. Lower costs leave more of your returns in your account, which can compound over time. For everyday investors seeking a straightforward way to participate in market growth without constant research or trading, index funds offer a simple, disciplined path aligned with long-term financial goals.

How Index Funds Work

Index funds aim to match an index by either fully replicating it or using a representative sample. Full replication buys every component, while sampling holds a subset that closely reflects the index's characteristics. Many equity index funds use market-cap weighting, giving larger companies a bigger presence and smaller firms a smaller one, which naturally shifts as markets move. Returns are never perfectly identical to the benchmark due to tracking error, a small performance gap caused by fees, trading costs, and timing. Managers perform periodic rebalancing to keep weights aligned with the index methodology. You can access index strategies as a mutual fund or an ETF. Mutual funds trade at the end-of-day price, while ETFs trade throughout the day at market prices, introducing elements like the bid-ask spread and premiums or discounts versus net asset value. Despite these mechanics, the essential goal remains consistency: deliver the index's performance, less minimal costs, with transparent, rules-based exposure.

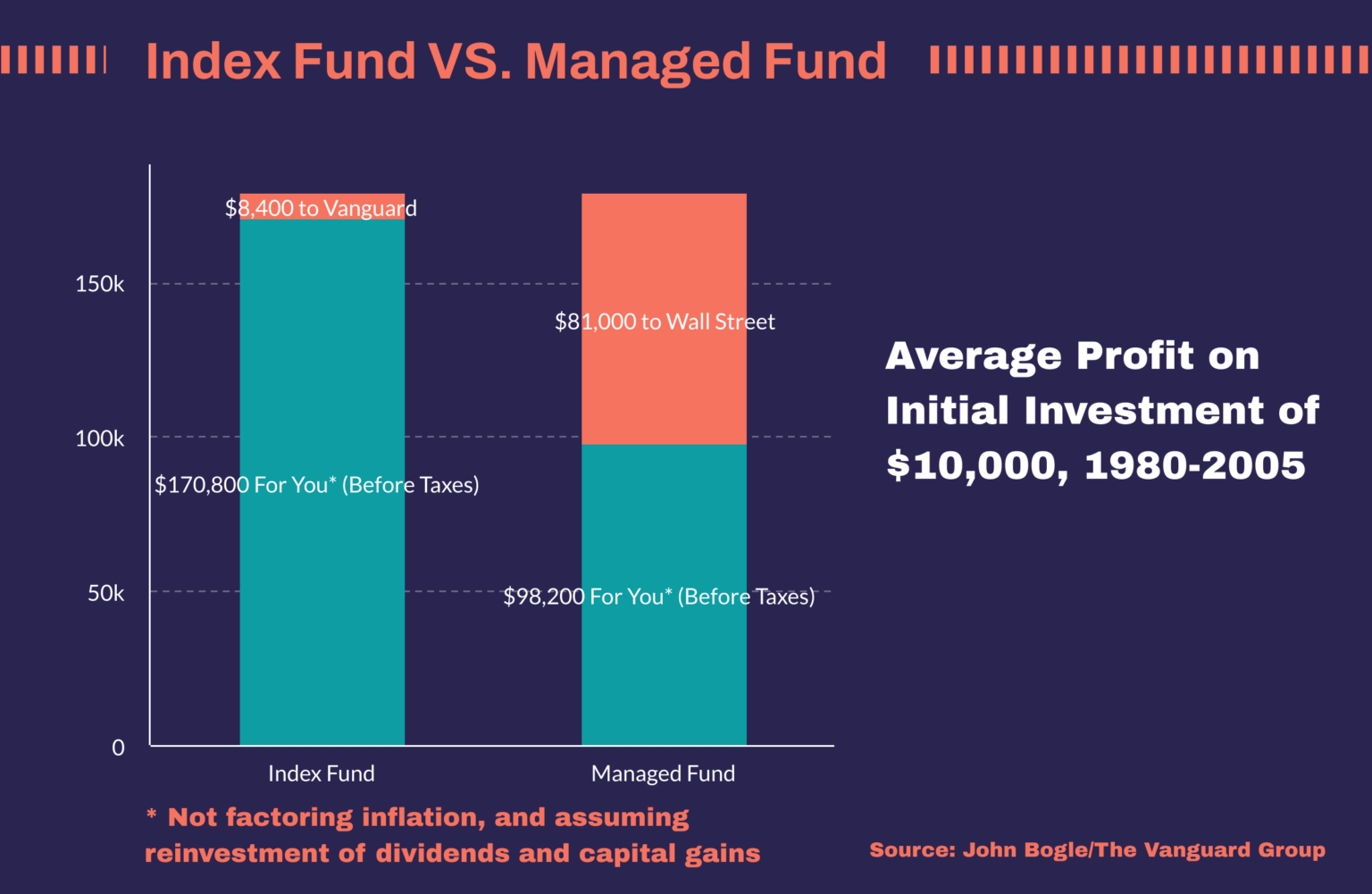

Why Many Investors Choose Them

Index funds appeal because they combine low costs, simplicity, and broad diversification in a single package. Keeping fees down is powerful, since expenses reduce returns every period; by minimizing frictions, more of the market's growth can reach your account. The approach is easy to understand and implement, which supports better investor behavior. When markets fluctuate, complexity can prompt second-guessing, but a rules-based index helps maintain discipline. Many index strategies are also relatively tax efficient compared to frequent trading approaches, which can help investors retain more after-tax gains depending on their situation. By owning large swaths of the market, investors capture the aggregate outcome rather than betting on individual winners. Over long horizons, consistency and compounding become key allies: even modest differences in cost or behavior can meaningfully influence results. For personal finance goals such as building wealth, funding education, or preparing for retirement, index funds offer a dependable foundation that aligns with patient, goal-focused planning.

Building a Simple Index Portfolio

A practical way to start is to design your asset allocation around just a few core index funds. A total market stock index can provide broad domestic exposure, while an international stock index adds geographic diversification. Pairing those with a high-quality bond index can temper volatility and support stability. The exact mix should reflect your risk tolerance, time horizon, and cash flow needs. Investors often automate contributions, a form of dollar-cost averaging that buys more shares when prices are lower and fewer when they are higher, creating a steady accumulation habit. Maintain an emergency fund outside your portfolio to avoid selling investments during downturns. Set clear rebalancing rules—calendar-based or threshold-based rebalancing—to keep your portfolio aligned with its target weights, trimming what has grown and adding to what has lagged. This simple, rules-driven structure reduces decision fatigue, supports consistency, and keeps your focus on long-term objectives rather than short-term noise.

Getting Started and Avoiding Pitfalls

Open an investment account with a reputable provider and identify index funds that fit your plan, paying close attention to fees, minimums, and tracking quality. Decide whether a mutual fund or ETF format suits your trading preferences, remembering that ETFs introduce factors like bid-ask spreads and intraday pricing. Automate contributions for automation and consistency, and document your rebalancing guidelines in advance. Common pitfalls include performance chasing, where investors switch funds after strong returns, only to miss future gains; overdiversification, which piles on overlapping funds without adding meaningful new exposure; and ignoring costs beyond the expense ratio, such as spreads and transaction fees. Recognize that volatility is normal; align your allocation with your tolerance so you can stay the course through market cycles. Keep the process simple, keep costs low, and keep behavior disciplined. Over time, that steady approach is often more influential than any single tactical decision or market forecast.